Post-M&A integration of the acquired corporation

Oktober 2019

Integration of the acquired corporation

Whereas the negotiation teams catch their breath and champagne is being poured after the closing of the M&A transaction, the actual work of the merchants and lawyers is still at the very beginning. The acquired corporation has to be integrated into the corporation of the buyer.

“Day 1”

Until the completion of the transaction, i.e. closing of the corporate acquisition, the operation is strictly confidential and only known by a small circle of involved persons. Shortly after closing, the restructuring has to be made public in a coordinated manner. This is commonly referred to as “day 1”, the beginning of a new time reckoning.

From a legal point of view, communication with the employees requires special attention. The Finnish Act on the involvement of employees in the decision-making processes of the company stipulates various requirements. Especially when the acquisition takes place in the form of an asset deal, the act defines specific information that needs to be submitted to the employee representatives partly even before the entry into force of the transfer.

Management of integration

The integration of the acquired corporation requires substantial management resources in a short time. If the necessary adjustments and restructurings are not implemented immediately after the corporate acquisition, valuable momentum is lost. If work continues as usual for a longer period of time despite the sale, later changes are harder to implement.

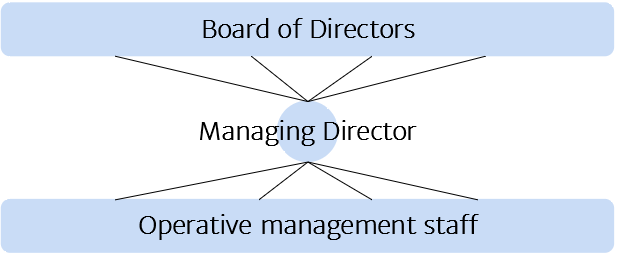

The company’s regular management may be overwhelmed by the burden of managing both the ongoing operations and the group integration at the same time. In a Finnish company, a single managing director is responsible for day-to-day business – further managing directors cannot be appointed. The board of directors generally focuses on a more or less active supervision, but bears own responsibility in case of far-reaching projects.

According to the basic concept of the Finnish corporation structure, a bottleneck can easily emerge as shown in the following graphic:

In order for the integration project to succeed subsequently to a corporate acquisition without business operations suffering from it, a clear responsibility should be defined. A new integration manager typically posted by the new parent corporation should take over the management and coordination of the integration during the “hot phase” after the closing.

If a Finnish company is acquired by a foreign corporation, posting of an integration manager is almost indispensable unless the target company’s management is replaced with posted employees altogether. The integration challenges regarding the administration, business philosophy and business culture are unequally higher in this case. These can only be conquered with intense personal presence on site.

In cross-border cases, local personnel tends to resist integration efforts claiming that accustomed working methods could not be altered due to legal regulations. Of course, such input should be taken seriously. Alignment of business practices without a review of the legal environment or also the local customs of the sector can do more harm than good. On the other hand, often enough such arguments are based on misunderstandings or pure defensive reflexes. These situations should be identified. Therefore, the integration manager should continuously be advised about the legal framework in Finland.

Relevance of integration in the transaction phase

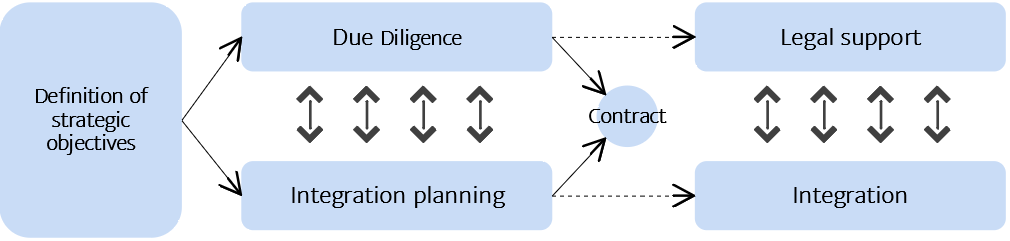

The chronology of an M&A project is often depicted in a simplified, yet misleading manner: commercial negotiations – due diligence – contract – integration. In fact, it would constitute a great danger to the success of an acquisition, if the subject of integration would only be addressed after the contract completion.

Due diligence is not a standardized procedure. It only gets its meaning through a close connection to the strategic goals that the purchaser pursues with the acquisition. Successful integration is a decisive prerequisite for the fulfilment of the strategic goals. Therefore, an appropriate due diligence scrutiny cannot be conducted without knowledge about how the acquired corporation should be integrated. On the other hand, the planning of the integration can in many ways only be conducted, if the key data of the due diligence is available.

This means that integration planning and due diligence have to be conducted in parallel according to the definition of the strategic aims. Hence, there has to be a continuous dialogue between the strategy planning team and the M&A team:

The conceptional cooperation in the transaction phase is mirrored in the execution of integration after completion of the acquisition. The operational merger of the corporations requires numerous legal individual measures. It makes sense to create a personal continuity between the phases in order to achieve an ideal execution. The integration manager should already be involved in the integration planning, the legal transaction team should also legally flank the conduct of the integration.

Post-M&A integration of the acquired corporation